Insurance protects individuals, families, and institutions from the full cost of an unexpected adverse event, such as crop damage, an automobile accident, or ill health. Insurance is a way to ”pool” funds so that the burden is not just on those who experience an adverse event; the financial risk is spread across a group where individuals or institutions face varying odds of an adverse event occurring.

Insurance involves prepayment, meaning those enrolled in insurance schemes pay “premiums” on a monthly or annual basis, or as a lump sum, to be eligible for future insurance benefits. Insurance may require copayment or include a deductible. Insurance prices are based on predictions of the frequency of uncertain, damaging events happening among the insured group. The lower the risk of adverse events in the ”pool” of insured people (e.g., mostly safe drivers), the lower the cost of the insurance.

What is health insurance?

Although no one plans to get sick, most people will need healthcare at some point in their life. Health insurance prevents people from having to pay out-of-pocket for the full cost of a health service at the point of service delivery. It is also characterized by established enrollment processes that dictate when, where, and how someone joins a scheme and a benefits package (i.e., a defined set of covered services) made available through accredited health providers who are paid in advance or reimbursed by the insurer.

Those who know they are already sick may have a stronger desire to buy insurance at an affordable price, while those who are healthier may have a lower incentive to buy insurance, as they do not perceive an immediate need. When only sicker individuals buy insurance, the pool of those insured is skewed toward a higher likelihood of payout for the insurer; this is called “adverse selection”. In order for a health insurance scheme to be sustainable, it needs to be affordable for those enrolled, and insurers need to be able to cover their operating costs. Therefore, health insurance schemes are most sustainable when there are a large number of participating individuals with varied risks of ill health, which may be based on a diverse demographic, socioeconomic, and disease-burden profile of the insured.

Governments can promote higher uptake of insurance by helping to bring down the cost of premiums. They can do this by subsidizing the premiums directly or by grouping large pools of the insured to reduce “fragmentation” (e.g., consolidating multiple schemes covering small segments of the total population). When there is a large pool of insured, cross-subsidization is more likely to occur, where the wealthier and healthier subsidize the costs borne by the poorer and sicker. In such a large group, there will be a mix of those who have a predisposition and higher risk for costly illnesses and those who are at lower risk. There will also be those who have higher income and can potentially contribute more toward their premiums and copayments than those who have less disposable income. Higher-income people will contribute more into a scheme if premium payments are based on a fixed percentage of monthly salary or a graduated scale of payments linked to income or wealth.

Types of health insurance schemes

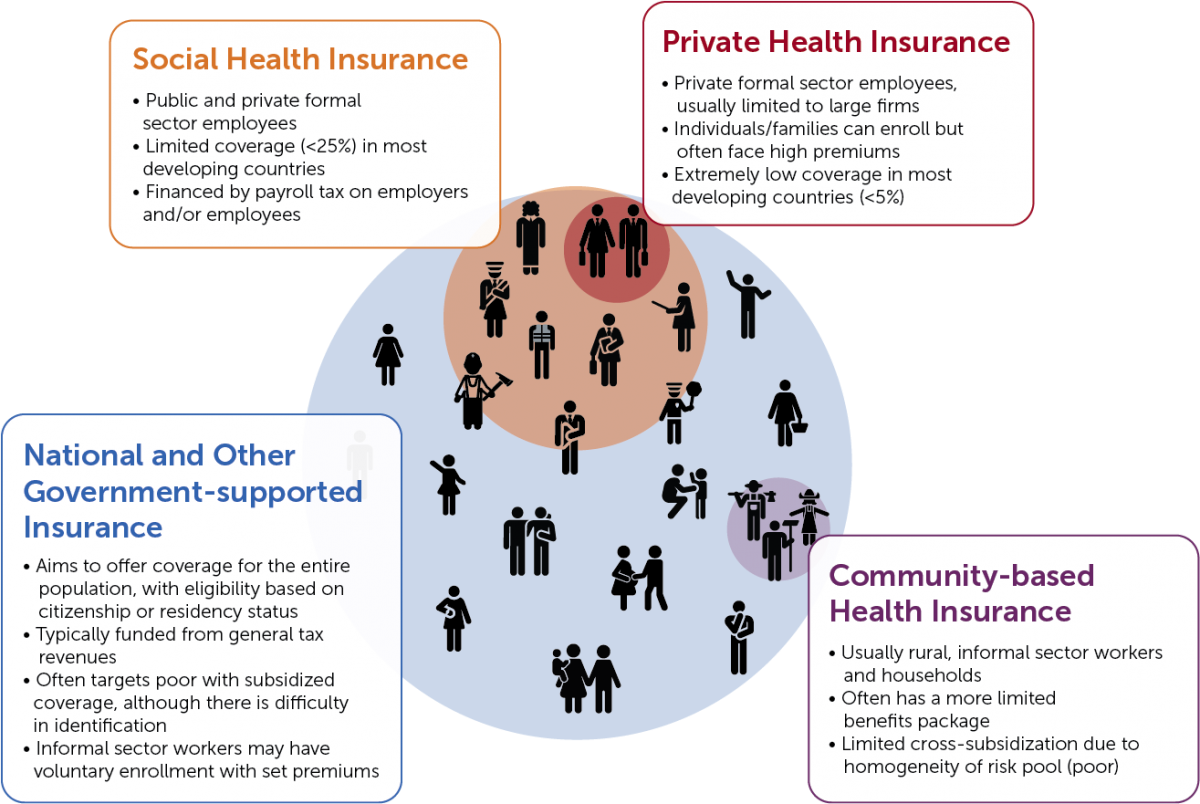

Health insurance schemes can be private or government-operated, cover different segments of the population, and offer varying premium payments and benefits packages. Below are descriptions of four overarching types of insurance schemes: national, social, private, and community-based (Figure 1).

Figure 1. Types of health insurance schemes

Government Health Insurance Schemes

The two main types of government health insurance schemes are social health insurance (SHI), which is based on the Bismarck healthcare system model, and National Health Insurance (NHI), which has some of the same components of a Beveridge healthcare system. Many countries have hybrid elements from both Bismarck and Beveridge models in their health insurance schemes, and the design of specific SHI and NHI schemes varies across countries. However, in most government health insurance schemes, a fully or semi-autonomous government institution administers enrollment, contributions, and payments.

The Bismarck model associates the right to healthcare with employment. This is the foundation of SHI, in which employees working in the formal sector (or their employers) contribute to the insurance scheme through mandatory payroll deductions. In some countries, enrollment might be limited to government employees, as it may be easier in certain settings to identify, enroll, and collect premiums from these individuals compared to those working outside of the government. Universal coverage is not the aim of SHI, and large segments of the population may be uncovered under SHI, particularly if more people work in the informal sector. As a result, many governments operate voluntary or subsidized schemes in parallel to SHI in order to make progress toward universal health coverage by increasing population coverage of health insurance and offering financial protection to the poor and vulnerable. In such cases, informal workers can voluntarily join the scheme and pay fixed or tiered premiums based on the class of care sought (e.g., inpatient wards vs. private rooms). Governments may partially or fully subsidize premiums in the voluntary scheme for poor individuals or households, which is the case in several countries (e.g., Costa Rica, Colombia, Ethiopia, and Indonesia). For these schemes, effective targeting of the poor is critical to ensure the correct households are identified for government subsidies. In many cases, the package of services in these schemes is identical to those provided by SHI, although it may be limited either in the services offered or the facilities that provide them.

Under the Beveridge model, exemplified by Britain’s National Health Service, healthcare is funded for the entire population through government tax revenue. The Beveridge model is a “single-payer” system where the government is the sole purchaser of health services. National Health Insurance is also a “single-payer” scheme that every citizen or resident pays into and is eligible to enroll in. Canada is an example of a country with this type of NHI system. Although a government may use tax revenue to subsidize an NHI scheme, insurance is distinct from health services financed by general tax revenues through line items in government budgets. Under an NHI system, the government may pay a health facility based on the number and type of services they provide or the number of people in the area served by the facility, whereas a government that finances healthcare through budget line items would pay facilities according to budget allocations based on trends in expenditure or other criteria.

Private Health Insurance Schemes

Private schemes typically enroll wealthier, formal sector workers, and premiums may be partially or fully subsidized by employers. Typically, any individual or household can enroll in these schemes, although enrollees often face high premiums and deductibles; individual enrollments thus represent a relatively small share of total enrollments. On the whole, private insurance coverage is relatively low, particularly in developing countries.

Community-Based Health Insurance

Community-based health insurance (CBHI) is mainly used to provide financial risk protection and improve healthcare access among low-income households in rural areas. CBHI usually involves voluntary membership that pools members’ premiums into a collective fund that is managed by the members. CBHI generally covers basic healthcare costs at local health facilities. CBHI has worked well in Rwanda, where insurance coverage among the CBHI target population increased from 7 percent to 74 percent from 2003 to 2013.

How Does Health Insurance Relate to Family Planning?

As some developing countries have “graduated” from donor support – and others face transitions in donor funding – the provision of family planning services may shift away from vertical programs and social marketing schemes toward integration of family planning into existing service delivery and financing systems. Including family planning in existing health insurance schemes presents an opportunity to ensure that adequate and sustainable financing is available for family planning.

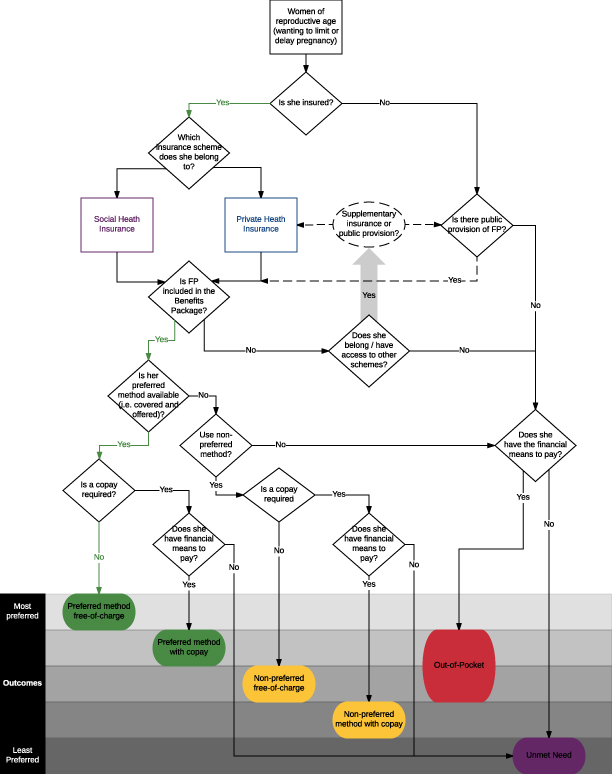

Health insurance could lead to increased uptake of family planning services, particularly more costly long-acting reversible or permanent methods, by reducing costs at the point of service for users. For health insurance to increase family planning uptake, schemes must meet a series of conditions (Figure 2):

-

Women and their partners must be covered by relevant schemes. In particular, these schemes must target those who lack the ability to pay out-of-pocket for family planning methods.

-

Family planning must be included in the benefits package, either explicitly listed as a benefit of a positive benefits package or not explicitly excluded as part of a negative benefits package.

-

The range of methods covered must be sufficient to provide selection among short-acting, long-acting reversible, and permanent contraceptive methods, to ensure that women and men have access to their preferred method.

-

Providers accredited to the schemes must have the ability to provide the range of methods covered, and be reimbursed appropriately for different method selections so as to incentivize (but not coerce) provision of family planning services.

-

Insurance must provide sufficient financial protection (i.e., no or low patient copays) such that the preferred method is affordable and does not present a significant financial barrier for women and their partners.

Countries in Latin American and the Caribbean have made significant progress in the past 30 years both in family planning prevalence and expansion of insurance coverage. In most upper-middle and high-income countries in the region (e.g., Chile, Colombia, and Costa Rica), social health insurance – either contributory or subsidized – now covers most people and includes a range of family planning services in its benefits packages. However, in low- and lower middle-income countries, social health insurance has not incorporated, or only partially incorporated, family planning benefits, and clients are forced to seek services in overcrowded and underfunded public facilities. While formal insurance coverage, through SHI or other related schemes, can provided improved and sustainable family planning service provision, such provision has not necessarily translated to fully satisfied demand for family planning. Efforts to expand insurance coverage must be complemented by efforts to address nonfinancial barriers – including cultural appropriateness of health services, and geographic access – to reach more and marginalized populations.

Kenya’s National Health Insurance Fund covers a range of short- and long-acting reversible methods under outpatient contracts. Providers are reimbursed a fixed amount per patient per year, regardless of whether the patient uses family planning (capitation). This may incentivize providers to provide short-term rather than long-acting reversible methods, as providers receive the same payment regardless of the method chosen and short-term methods tend to be simpler and less costly. Permanent methods are covered under inservice contracts, and providers are reimbursed for each service they provide (i.e., fee-for-service).

The NHIF has had limited success in targeting and enrolling the poor, meaning NHIF may not have increased uptake of family planning among underserved populations. Further, there are still issues regarding commodity availability, provider capacity, and other health system constraints at the point of service delivery, hindering expansion in family planning access.

Resources

The purpose of this guide is to provide practical action steps that public health insurance agency staff can take to improve the sustainability of

L’objectif de ce guide stratégique est de présenter les mesures concrètes et pratiques que le personnel des agences publiques d’assurance maladie

The Royal Government of Cambodia recently launched its National Social Protection Policy framework to strengthen and expand social security and

Building off previous HP+ analyses in Latin America and the Caribbean region, we examined whether the inclusion of family planning services in

This report summarizes the results of a literature review and expert consultation conducted to support the definition of family planning benefits